{kind=link}

E-mini-Nasdaq 100 Futures reached a new all-time high of 22,901.50 on Friday and are currently trading near those prior highs. See our previous analysis here: Clear Path towards New All Time Highs E-mini S&P 500 Futures are approaching their all-time highs, while Futures continue to lag, currently down 3.73% year-to-date (YTD).

Source: Finviz (As of 03:45 AM CT)

The ‘Year-to-Date Performance’ data shows a range of asset behaviors. Notably:

- The USD is down 9.93% YTD.

- Energy is also down YTD, contributing to inflation stabilization, though it remains above the Fed’s 2% target.

- Precious and industrial metals: Platinum, Palladium, , Gold, and Silver are among the top performers.

- G10 FX futures have broadly outperformed the USD, with EUR leading, up 12.06% YTD.

- market cap has recovered to its peak of $54.6 trillion.

Key Questions for H2 2025

What are the expectations for:

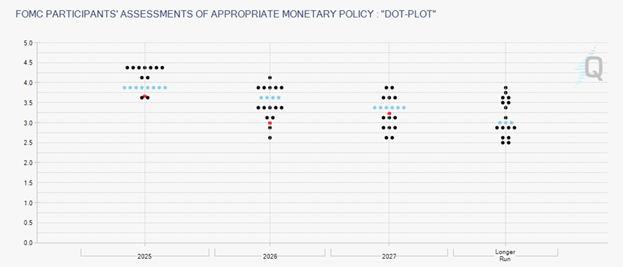

Federal Reserve’s June 2025 Dot Plot

Source: CME FedWatch

Fed officials remain reluctant to cut rates, citing concerns about tariff-induced inflation potentially emerging in the coming months. According to the dot plot, the median forecast suggests the federal funds rate will fall to 3.9% by year-end 2025, implying two 25 basis point cuts.

However, the outlook among officials is mixed:

- 7 participants expect rates to remain unchanged (up from 4 in March).

- 2 participants expect one cut.

- 8 participants expect two cuts.

- 2 participants foresee three cuts.

Expectations for rate reductions in 2026 and 2027 are murkier and uncertain.

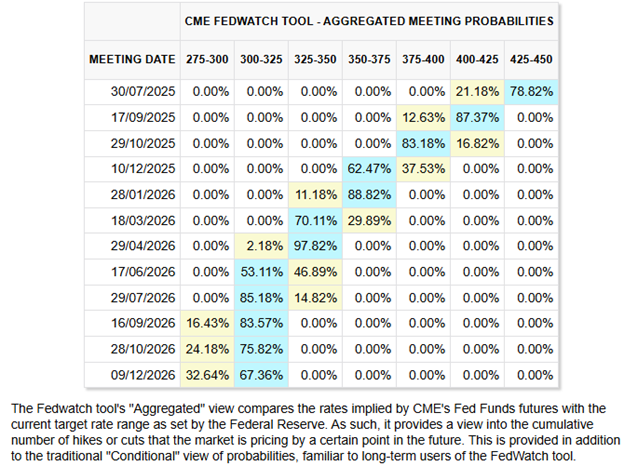

Market vs. Fed: Diverging Rate Expectations

Source: CME FedWatch

The CME FedWatch Tool indicates that markets are pricing in:

- Two 25 bps cuts by October 2025.

- 65% probability of a third 25 bps cut by year-end.

- By end-2026, rates are expected to be around 3.00-3.25 % level.

Notably, most Fed officials have adopted a more hawkish tone ahead of the July 2025 meeting except Governor Waller. Market sentiment is increasingly influenced by expectations that President Trump may appoint a more dovish Fed Chair.

Morgan Stanley sees a higher chance of no rate cuts in 2025, with bigger and more cuts in 2026. They cite tariff induced inflation in the near term, with weaker consumer spending with a lag. They expect higher prices with tariffs translating into a consumption tax. Stanley’s Global Head of Macro Strategy Matt Hornbach expects that the Fed will see more inflation before seeing a weaker labor market.

Government Debt and Monetary Policy Pressures

The cost of debt service is now the third-largest government expenditure, a whopping $1.03 trillion surpassing defense spending. With U.S. national debt exceeding $37 trillion (Source: US Debt Clock), President Trump is advocating for lower rates to facilitate refinancing at reduced costs.

Fed’s Updated Economic Projections

- Real GDP growth for 2025 has been revised down to 1.4% (from 1.7% in March).

- The PCE inflation forecast was revised up to 3.0% (from 2.7%).

These revisions point to stagflationary pressures, as both growth slows and inflation persists.

Fiscal Policy: Trump’s BBB Bill and Debt Implications

The Senate is set to vote today on President Trump’s sweeping tax cut and spending bill, following a narrow 51–49 vote to open debate. The Congressional Budget Office (CBO) estimates that the Senate version of the bill would add $3.3 trillion to the national debt over the next decade.

Although trade deals are adding to market optimism, many overlook that the effective tariff rate on China has reached 55%. The bill’s passage could fuel further inflation while adding to government debt. July 9th tariff deadline for many countries approaches. However, as previously noted, the worst is behind us and we expect Trump to not chicken out but reshape how tariffs are viewed by aggregate participants.

Key questions remain:

- Will higher tariffs translate into greater government revenue?

- Can reshoring production and domestic industrial policy materially boost GDP?

The U.S. appears to be transitioning from globalization to strategic de-globalization, not full decoupling, but certainly a “Modern Mercantilist” approach echoing the term cited by Bridgewater Associates.

Geopolitical Landscape

Middle East:

A fragile Iran–Israel ceasefire holds. However, risks of preemptive strikes on Iran persist, particularly considering IAEA Chief Grossi’s recent statement that Iran could resume uranium enrichment sufficient for a bomb within months (Source: BBC).

Eastern Europe:

No ceasefire has materialized between Russia and Ukraine. The conflict is likely to persist as Russia sees no benefit in a ceasefire without key demands being met.

NATO Summit:

NATO members have committed to increase defense spending to 5% of GDP, divided as follows:

- 3.5% for core defense.

- 1.5% for defense-related expenditures, including support to Ukraine.

Progress on the 5% target will be reassessed in 2029.

Asia:

China hosted the Shanghai Cooperation Organization (SCO) summit with 10 member states, including Iran, India, Pakistan, Russia, and Central Asian nations, focusing on regional stability and counter-terrorism efforts.

Closing Thoughts

We are clearly entering an era of shifting alliances and multi-polar complexity. Global order is evolving, and discerning truth from propaganda is increasingly difficult. For market participants, price action remains a critical guide as markets often price in new developments before they reach the public domain.

***

Disclaimer: Derivatives trading involves a substantial risk of loss. Past performance is not indicative of future results. Any example trades are not inclusive of fees and commissions.